Many buyers are sitting on the sidelines waiting for mortgage rates to drop into the 5s. The instinct makes sense. Everyone wants a better rate.

But hitting 5.99% isn’t the unlock people think it is.

Affordability is still tough, but the market has already delivered a meaningful break. Rates peaked above 7% in May and have been easing ever since. That shift, small as it sounds, already translates into real savings.

What You’ve Already Gained Without Noticing

When rates slid from above 7% to the low 6s, the typical monthly payment for a $400,000 home fell by nearly $400 (source: Redfin). That’s a bigger improvement than most buyers expect, and it’s already on the table today.

If you paused your search earlier this year, the current numbers work out noticeably better. Waiting for something “dramatic” isn’t the only path forward.

Where Rates Are Expected To Go

Most forecasts show rates staying close to current levels through 2026. Only one major outlook calls for anything in the upper 5s next year. And even if rates do slip below 6%, the financial impact is smaller than many expect.

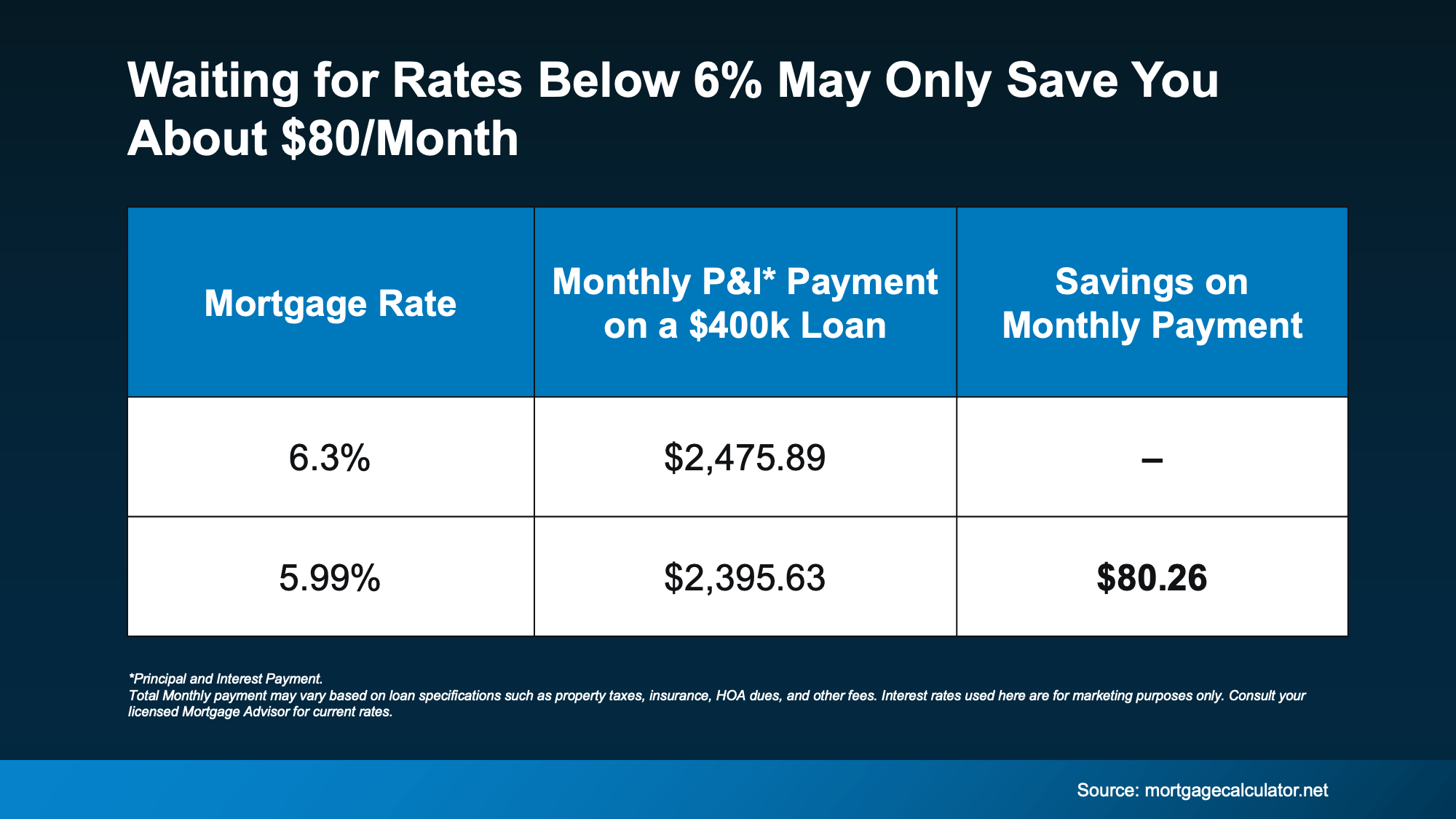

The Actual Math on 5.99%

Dropping from today’s low-6 range to 5.99% saves the average buyer roughly $80 per month. That’s it. Compare that to the nearly $400 in savings we’ve already gained since May.

So the real question becomes: is holding out for $80 worth what you’re risking?

What Happens When Rates Dip

Once rates start with a 5, even barely, buyer psychology shifts. More households suddenly qualify. More buyers re-enter the market. More competition appears overnight.

According to the National Association of Realtors, a drop to 6% opens the door for roughly 5.5 million additional households to afford the median-priced home. Even a modest percentage of those buyers jumping in means stiffer competition and upward pressure on prices.

That small rate savings can disappear quickly if prices rise.

The Bottom Line

You don’t need to wait for 5.99%. The meaningful savings have already happened. If the numbers work and you find a home that fits your life, the smarter move may be getting ahead of the crowd, not waiting for it.

If you want a clear picture of how the current rates affect your monthly payment, let’s run the scenarios.

>

> >

>